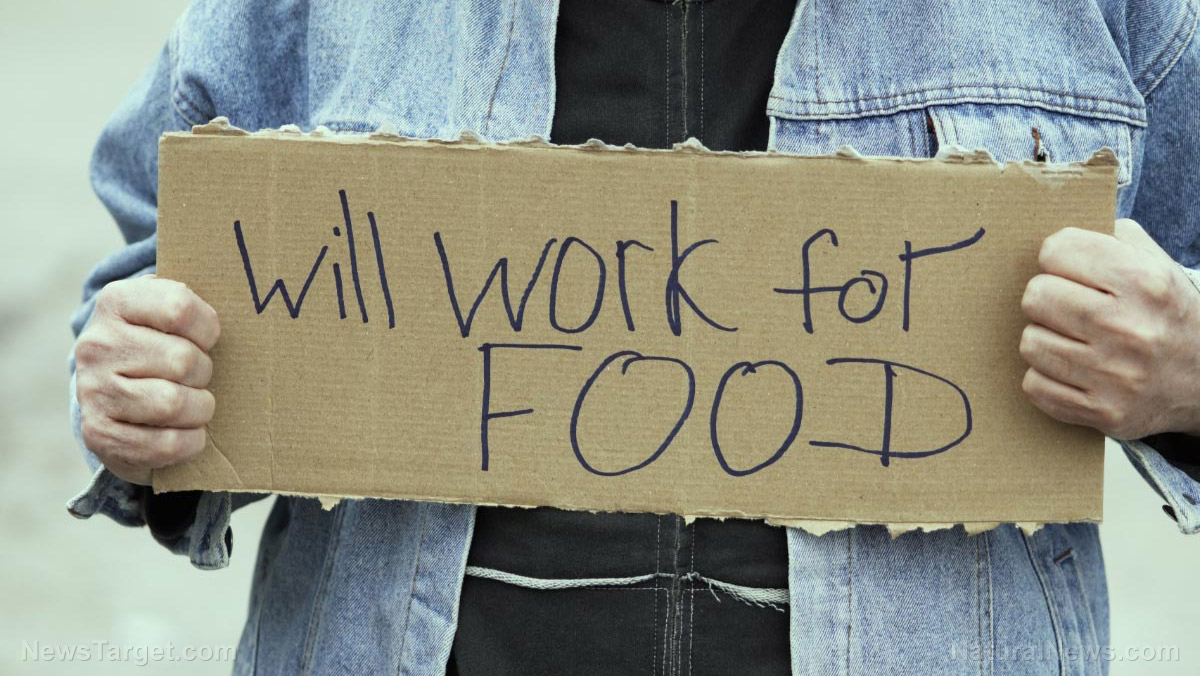

To continue buying groceries and gas, some Americans are having to take out micro-loans

07/14/2022 / By Ethan Huff

Swedish fintech company Klarna Bank is seeing increased demand for micro-loans from cash-strapped Americans who are no longer able to afford basics such as food and gas amid skyrocketing inflation.

The company says it has seen a flood of applications in recent days for staple items that people need just to survive, as opposed to the usual “luxury” items such as smartphones and other consumer electronics.

Klarma provides interest-free loans that allow borrowers to spread their payments out over multiple installments. The company makes money by charging retailers who offer the service to their customers a small per-transaction fee, as well as interest on longer-term loans.

“I noticed that I could buy essentials with it, and not have to pay everything up front – and it wouldn’t affect my pocket as much,” says Linda Cruz, a 37-year-old mother of four who lives near San Antonio.

Cruz started out using Klarna just for occasional larger purchases, including for a new air conditioning unit to replace her old one that died last summer during a heat wave. As cost of living continues to soar, however, she is having to use the loans even for groceries.

Will Klarna survive the shift in how people use its credit?

Klarna was apparently never prepared to offer loans for these types of things, and is now shedding hundreds of millions of dollars per quarter on them. According to reports, this makes the company more vulnerable to defaults from struggling customers who live paycheck to paycheck.

“This puts pressure on the Klarna model,” warns John Colley, a professor at the Warwick Business School. “Klarna will be sat there with substantial bad-debt risks. Their customer base is likely to be sub prime anyway.”

Klarna’s valuation is dropping as it tracks with the meltdown in capital markets. The company is “particularly vulnerable because higher interest rates, aimed at curbing inflation, boost its own borrowing costs.”

Klarna does not disclose its default rate, according to a company spokesperson. However, it does evaluate customers’ ability to repay on every transaction, and consistently keeps its losses at less than one percent.

As interest rates rise, however, Klarna’s cost of borrowing has risen sharply. The company’s two-year borrowing cost is now above four percent, which is more than double what it was at the beginning of the year.

This is what you call a meltdown in motion. Cheap and easy money from the Federal Reserve’s printers seems to be coming to an end, and the timing could not be worse for struggling Americans who are no longer able to put food on the table without extra help.

“The risk that you are building up is a debt problem that could be exacerbated by the cost-of-living crisis,” says Sue Anderson, an official with the debt charity StepChange, which along with Barclays bank found that 36 percent of users say that micro-loans have become a whole lot more appealing amid record inflation.

“People don’t see it in the same way they see other types of borrowing. It is marketed as interest-free, but that doesn’t mean it is risk free.”

It seems the Ponzi scheme of central banking might be coming to an end, which means things are going to get really ugly for everyone once the house of cards collapses.

The globalists think they have this one in the bag, presumably, but little do they know that ushering in their new world order to replace this collapsing system might not go as they plan.

“You know your government doesn’t care about you,” wrote a commenter. “They gave 56 billion to foreigners and gave you the bill, while you are starving.”

More related news about the downfall of civilization under the central banking Ponzi scheme can be found at Collapse.news.

Sources for this article include:

Submit a correction >>

Tagged Under:

capital markets, central banking, Collapse, cost of living, currency, debt, economic collapse, economy, fiat currency, gas, globalists, great reset, groceries, Inflation, micro-loans, panic, Ponzi scheme, poverty, risk, Tyranny

This article may contain statements that reflect the opinion of the author

RECENT NEWS & ARTICLES